A financial instrument which not only rewards you for spending money but also provides interest free credit period - no wonder why the Credit Card and the fintech industry is booming like anything. Given the Indian credit card industry is forecasted to grow at CAGR of more than 25%, we did an analysis of the existing players and their grip over the market. Below is a an interactive Tableau dashboard, which we have created with the publicly available data on RBI's website.

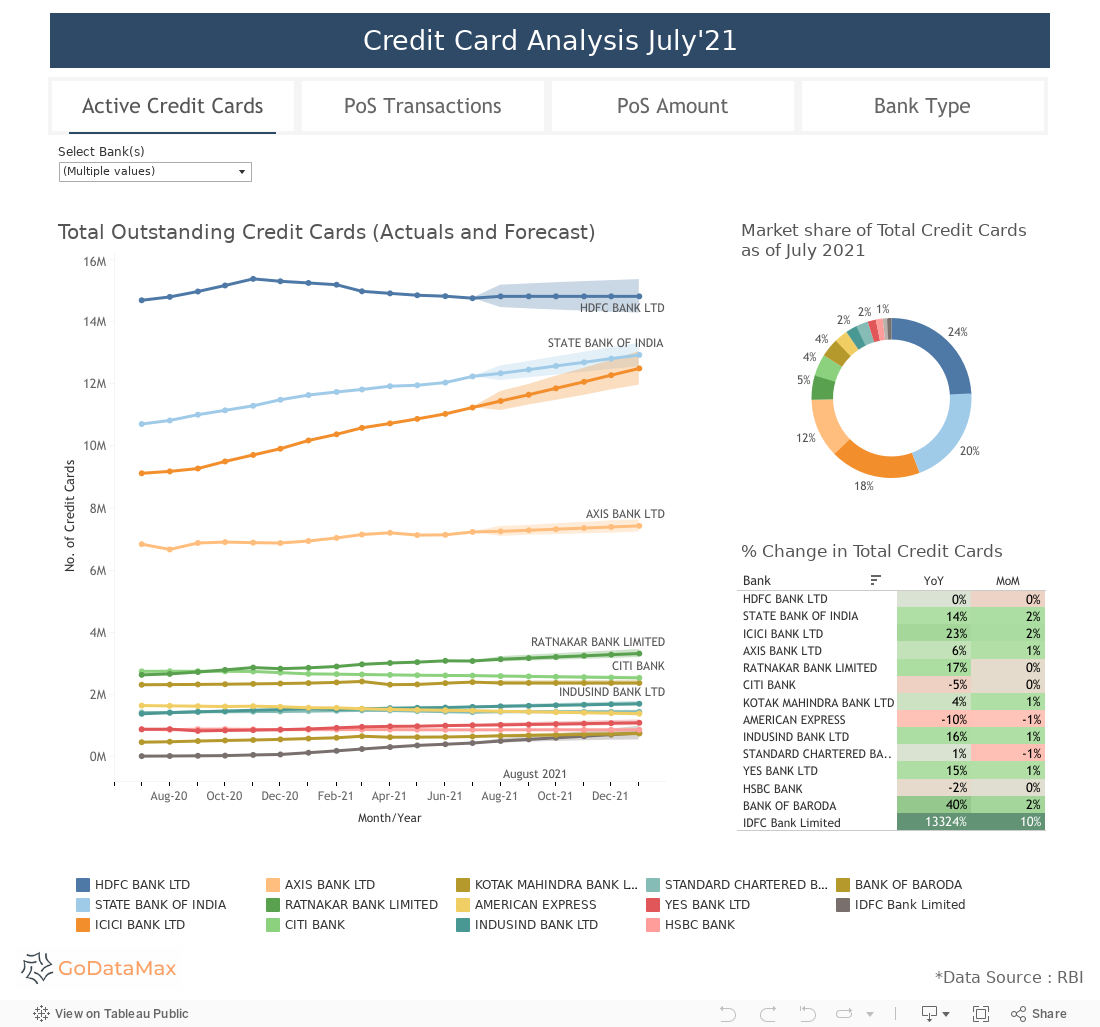

Active Credit Cards

HDFC is the clear leader in respect of the number of outstanding credit cards as of Jul'21 which stands at 14.7M. This is despite the fact that the bank was banned from issuing new credits for a period of 8 months beginning Dec'20 which led to a declining trend as seen below.

The ban on HDFC was cherry on the cake for it's competitors especially SBI, who had recently came up with it's IPO and ICICI, the bank holding the sweet third spot. If we look at the forecasted number of credit cards for SBI and ICICI, we can see a very close competition due to 9% higher YoY growth denoted by ICICI (Please ignore the HDFC forecasted numbers as the ban has just been lifted in Aug'21 and the data needs to be adjusted for correct forecasting). One of the possible reasons for this can be attributed to the lifetime free offerings along with Amazon branded credit card presented by ICICI but are missing in SBI's portfolio.

Next in the queue is Axis bank, which has showed a constant but a slow growth of 6% YoY despite a great portfolio catering to different sectors and audiences (not to forget the Flipkart branded card to counter ICICI's Amazon). It's important to note that there are no competitors within 3 million deviation which poses no immediate threat to it's position but at the same time would require immense efforts and perhaps, a change in the strategy to get to the top 3.

Coming to the next, Ratnakar bank (popularly known as RBL), holds the 5th position with about 3 million outstanding credit cards as of Jul'21 and a 17% YoY growth. The bank has gained a spot and outperformed CITI within an year. The negative growth rate of 5% YoY for CITI bank can be attributed to the fact that the bank announced the agreement to sell its consumer business in India, although it's yet to strike a deal.

Next comes the Kotak Mahindra Bank showing a stagnant growth which is perhaps due to the unattractive range of cards and offers. It is a bit surprising that the growth the bank has shown in last few years couldn't be seen in its credit card department.

Another surprise is for the American Express, the most elite credit card provider which witnessed a 10% decline YoY (partly due to RBI ban in Apr'21) and was overtaken by Indusind Bank which had a 16% YoY growth.

The next and the most promising entrant as of now look IDFC First Bank. With its lucrative offers, low interest rates, and lifetime free credit cards - it has taken the market with a bang and is witnessing a steep growth. It is interesting to note that the bank has also tied up with startups like OneCard, India's free metal card.

PoS Transactions

If you go to the next tab in the dashboard below, you'd see that although Citi bank has had a stagnant growth, it is a leader in average PoS (Point of Sale) transactions which sits at 4.7 per credit card for the month July'21. Citi is followed by IDFC First bank and is not a surprise given it's a new entrant with highly active users.

Although, HDFC and SBI hold the 3rd and 4th spot respectively in terms of average transaction per credit card - if we talk about the total number of transactions in the month and the market share, HDFC is the leader followed up by the SBI.

PoS Amount

Who do you think is the leader in terms of average spendings per credit card? No, unfortunately this is not bagged by AmEx but rather Indusind Bank which sits at Rs. 20,900 being spent in July'21 per credit card on an average. It is followed by IDFC First and American Express with Rs. 17,000 and Rs. 15,200 expenditure per credit card.

From market share perspective, HDFC again leads the chart with the most spendings in July'21 with a market share of 27% followed by SBI and ICICI at 19% each. All banks witnessed progressive YoY growth in terms of total amount spent with ICICI and Indusind outperforming most of the players.

The upcoming months would be even more competitive with the coming up of fintech startups like Slice and Unicard while allow the users to split the payment in three months without any extra charges.